In late October 2019, I authored an AdMonsters article with a list of existing, new, and soon-to-launch streaming services showing how they fit into the OTT ecosystem. Then, Covid-19 arrived and the migration that might have taken years took place in months.

Since then, due to the dramatic growth of CTV subscriptions and CTV ad spending within the larger definition of OTT (OTT includes viewing on any device, while CTV is content delivered through Smart TVs), this update will focus on CTV. Innovid defines the differences between OTT and CTV here. Now 53% of video viewing on all devices according to eMarketer | InsiderIntelligence is on CTVs. This will provide an update on CTV growth, a revised roster of CTV players, and what it means for Ad Ops.

Two CTV Business Models: Ads, Subscriptions Both Drive Revenue Growth

Brad Adgate in Forbes provides tracking and forecasts for CTV ad spending that show it is now “The Fastest Growing Video Advertising Platform.” Why? The value of CTV in delivering younger audiences and cord cutters as well as the potential to measure CTV impressions in ways that other digital ad platforms do.

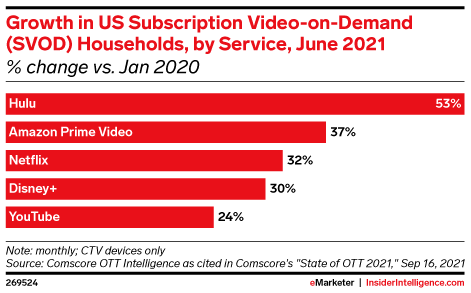

According to eMarketer | InsiderIntelligence, in 2022 the top five subscription services represent nearly three-fourths of total CTV viewing time.

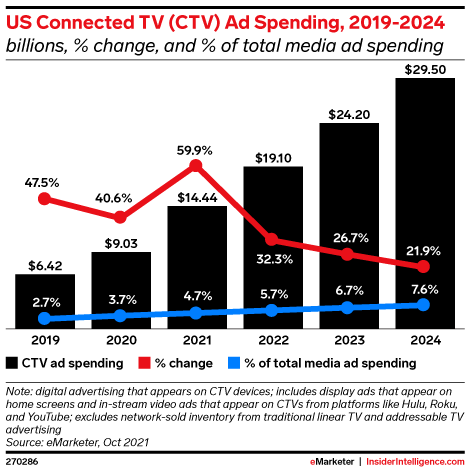

The CTV Advertiser: Ad Spend Trends

Insider Intelligence/EMarketer reports that “CTV ad spending is riding a wave of consumer adoption and platform launches. By 2025, spending will reach $34.49 billion, more than double the 2021 total of $14.44 billion.”

The CTV Consumer: Time Spent Viewing

Several major streaming services saw double-digit growth in viewing time, with Netflix, YouTube and Hulu experiencing increases of 26%, 21%, and 13% year over year, respectively.

Important CTV Developments For Ad Ops to Follow in 2022

There are three major areas of focus, that also offer many question marks when we talk about the continued healthy growth of CTV. People in Ad Ops must keep abreast of the many opportunities and fast-moving changes ahead:

Cross-Platform Measurement/Targeting, Reach/Frequency Management, Viewability, Verifiability & Attribution

Prohaska Consulting declares “Cable is the new landline and CTV is *very* hot (and very complicated)”, but sees movement in audience measurement/targeting from traditional TV HH metrics to more digital-friendly granularity: “This year, a few players debuted solutions designed to bridge the data and measurement gap and speed the migration of media to CTV. Nielsen announced Streaming Signals, a new offering that uses machine learning to identify individual household viewers and serve personalized ads accordingly.”

Mitch Oscar, Director, Advanced TV Strategy, USIM, is quoted in the Forbes Adgate article: “Nielsen still is the dominant measurer and reporter of campaign viewership. Hopefully, with the spate of recent announcements … offering solutions for … individual impression delivery versus reliance on panel modeling, … companies such as 605, Comscore, iSpot.tv, TVSquared, and VideoAmp will glean the support necessary to move from aggrandizement to the heavy lifting – sales lifting that is.”

Brand Safety, Data Privacy, and Fraud Security

Ad Ops will be integral in staying on top of these issues, especially now when 70% of CTV is purchased programmatically (per eMarketer | InsiderIntelligence). According to Comscore, by the latest count, there are at least 130 CTV apps in the market with many more to come. Each needs to be able to address these areas of concern efficiently and with integrity.

Cross-Platform Buying and Dealing with “Walled Gardens”

Advertisers and agencies need more efficacy and brand safety in dealing with buys from multiple DSPs as well as direct sales, as several CTV platforms seek to become walled gardens like Apple, Google, and Facebook. Moving from the GRP-based buying currency of traditional TV to targeted impressions will be important for cross-channel advertiser buys and reporting analytics.

SUMMARY

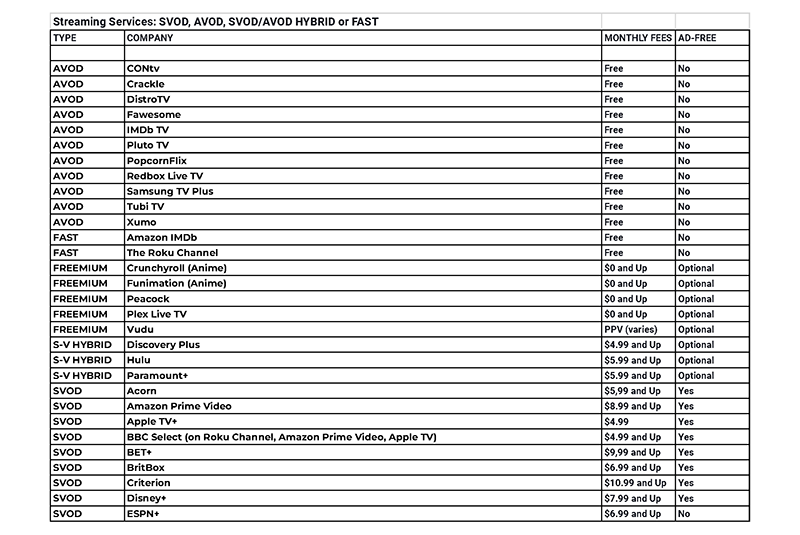

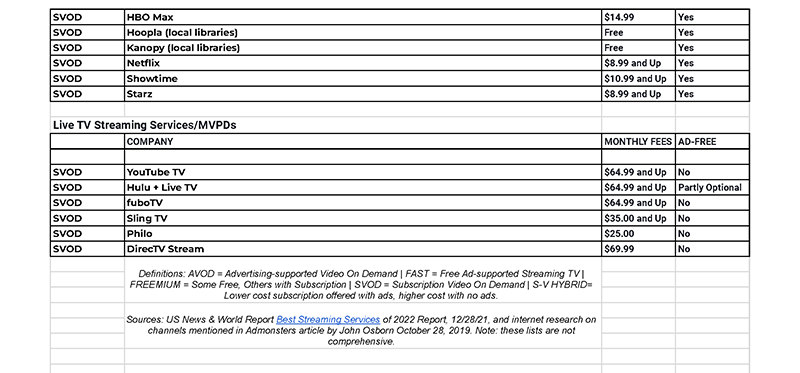

A February 2022 Update on Streaming Services by Type, Consumer Cost and Role of Ads